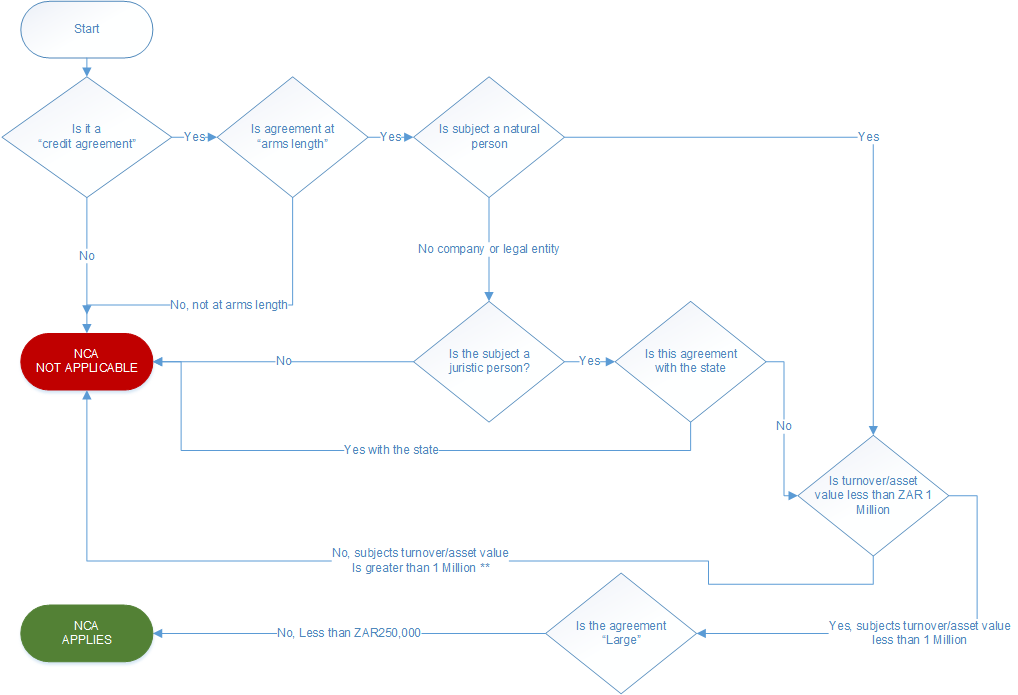

The National Credit Act was passed mainly to protect the consumer. It applies to all juristic persons (with limitations) and to all natural persons (even if they are a sole proprietor). It also applies to trusts that have two or fewer trustees (unless one of the trustees is itself a juristic person). The NCA does not apply to large juristic persons, that is those that have an annual turnover or asset value in excess of ZAR 1 000 000 (one million)

“Small transaction” – principle debt of less than or equal to ZAR 15,000

“Medium transaction” – principle debt of between ZAR 15 000.01 and ZAR 249,999.99

“Large transaction” – principle debt greater than or equal to ZAR 250,000

“State” – Part of government of Republic of South Africa

“Arms length” – An arm’s length transaction is a transaction in which the buyers and sellers of a product act independently and have no relationship to each other. The concept of an arm’s length transaction is to ensure that both parties in the deal are acting in their own self interest and are not subject to any pressure or duress from the other party.

“Credit agreement” – In order for the agreement to be classified as a credit agreement for purposes of the NCA, it must have two essential elements: credit must be extended; and there must be a fee, charge or interest imposed for deferred payment, or a discount must be given when prepayments are made.

“juristic person” – The Act defines a juristic person as a partnership, association or other body of persons corporate or unincorporated. A juristic person under the Act would include a trust with more than two trustees or where a trustee is itself a juristic person but not a sole proprietor.

“subject” – The person/company in question

Exclusion

True rental agreements are not credit agreements for the purposes of the NCA. This means that a consumer entering into a true rental agreement is not governed by the NCA. Must carry a true residual value

Large transactions

State

Following provisions of the Act do not apply to juristic persons/consumers:

Over-indebtedness and reckless credit.

Credit marketing practices.

Illegality of variable interest rates, except if pegged to a reference rate such as the prime overdraft rate.

Limitations on credit charges (particularly the prohibition on interest not exceeding the capital sum owing).

How To Decide ?

Follow the decision map to get your answer.

Tips

** Do you have sufficient proof the turnover or asset value is less than ZAR 1 Million

Quick Guide To Direct Marketing Compliance With introduction of POPIA (Protection of Personal Information Act) one of the major changes is the way we market to current...

We use cookies on our website to give you the most relevant experience by remembering your preferences and to analyse traffic. By clicking “I Accept”, you consent to the use of ALL the cookies used. Read our Privacy Policy for more information.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

{kind=link}