- Login

Login

Welcome back

Let's make today a great day!

Don't Have An Account Yet? Signup for free! - Who we are

- What we do

- Customer stories

- Contact us

- Login

- Sign up

- Enquire Now

It is said that when we look at things in different way that we can change our entire perception, and yes, they are right. Take for instance, if we simply accept uncertainty it then becomes an adventure and no longer uncertainty. Accepting the good in others suddenly changes envy to inspiration. In the same way as accepting what is beyond our control changes anger to tolerance.

So why not look at credit limits and management differently? After all, you are essentially extending credit (money) to a customer for a period, with no interest! This scenario highlights that you are a very generous person but it can place you in a position which makes you feel bad asking for your money when it is not paid back to you in time.

This incidental credit agreement usually happens without any background credit vetting or any other formal process, simply the “way it is done” so no process or policy is followed. Generally, the incidental credit agreement involves business with an individual or individuals we know or that we got introduced to at a point in time. When I ask somebody how they gave that individual a credit limit and on which terms they did, the answer is usually the same. “I know him and he is a great person”; we’ll call him Joe for now, and the amount was simply what Joe needed to fulfil the order. This practice of self-handling credit is very dangerous for numerous reasons which I will elaborate on later.

Offering clients payment terms has become a somewhat de facto standard of business operations globally but why is this the case? To a large degree it has happened as an unintended consequence due to the simple fact that formal lending from banks, for example, is becoming increasingly difficult to come by. As a result of this, businesses have created a way of helping each other’s cashflow by offering payment terms to help manage cashflow with the average payment term being 30 days. This payment term means the customer has 30 days to pay you for products and services offered to them.

If we look at this system of mini loans between companies, we can clearly see how closely inter-related industries and businesses become and the knock-on effect that happens when one business fails or fails to meet its obligations to the next one.

Getting back to Joe, and the danger of this informal lending along with all the problems it creates. So, let’s take the scenario of Joe. Joe doesn’t pay you on day 30 after the invoice was issued. No concern yet as you think he will see to the payment soon. Then shortly, day 40 arrives and still no payment has been made and you decide to call Joe. Joe confirms he will make payment soon and you take his word for it, worry averted you naively think. The following week you still do not have the money owed, so you call Joe again and the conversation becomes more awkward. He now tells you about his cashflow issue since he did not get paid for a large contract but assured you his payment is coming soon. By now you start sweating. It is day 60 and still no payment. You have already paid your overheads and your suppliers which results in you battling with cashflow yourself since all your cash is tied up in those invoices. By now it should be clear to see how problems have escalated and there is no policy to manage it. The real question is whether Joe was even good for the amount from the start? Did he have financial problems before you started to trade with him? All these questions were unanswered since no formal policy exists and no credit vetting took place to verify information and if Joe, the customer, has a clean credit profile.

Now with that said, a lot of people say I am too small for a credit policy or process, and they are wrong. According to research done in the US, which we can arguably consider a developed market, only around 20% of companies have a formal credit policy. As a side note, quality formal research in South Africa does not exist on this but I do expect this figure to be far less with regards to having a formal policy. Now of those companies with a formal policy, 19% update and review it every 2 years or less, 13% every 3 years and 15% when its required and the rest well you guessed it don’t really look at it again. What is even more staggering and rather surprising is that only around 40% of business use an accounting system of sorts to manage clients, invoices, quotes and credit limits and terms the rest is on paper or famous Excel or even worse nothing.

How can you change this you may ask? Easy, let us assist you as after all it is what we do and we can guide you on this journey.

Cred-it-data can assist you to:

Products we offer to assist you in doing some formal credit assessments starting at only a few rands:

For more information about how Cred-it-data can assist your business during these unusual times with no monthly fees, contact us today on +27861 22 22 10 or email us on support@creditdata.co.za.

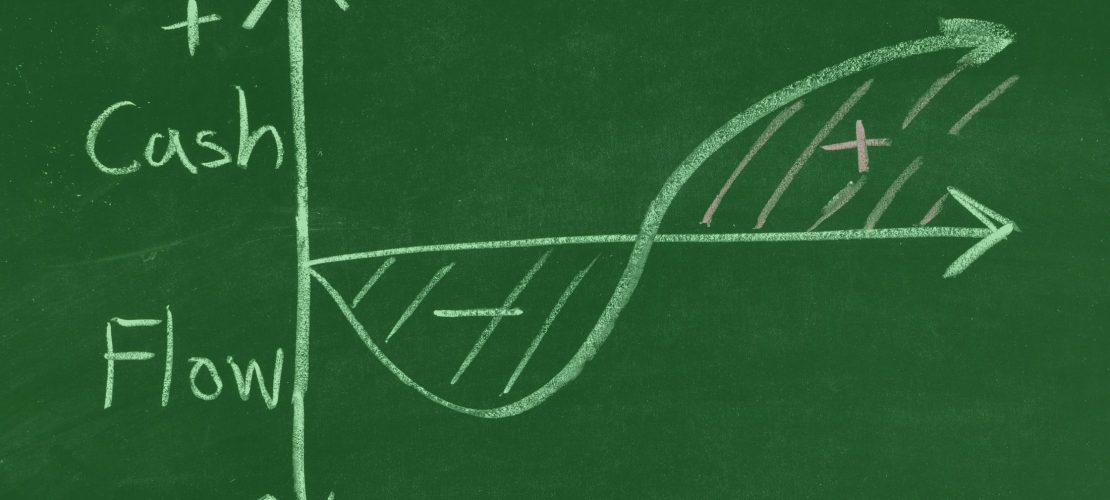

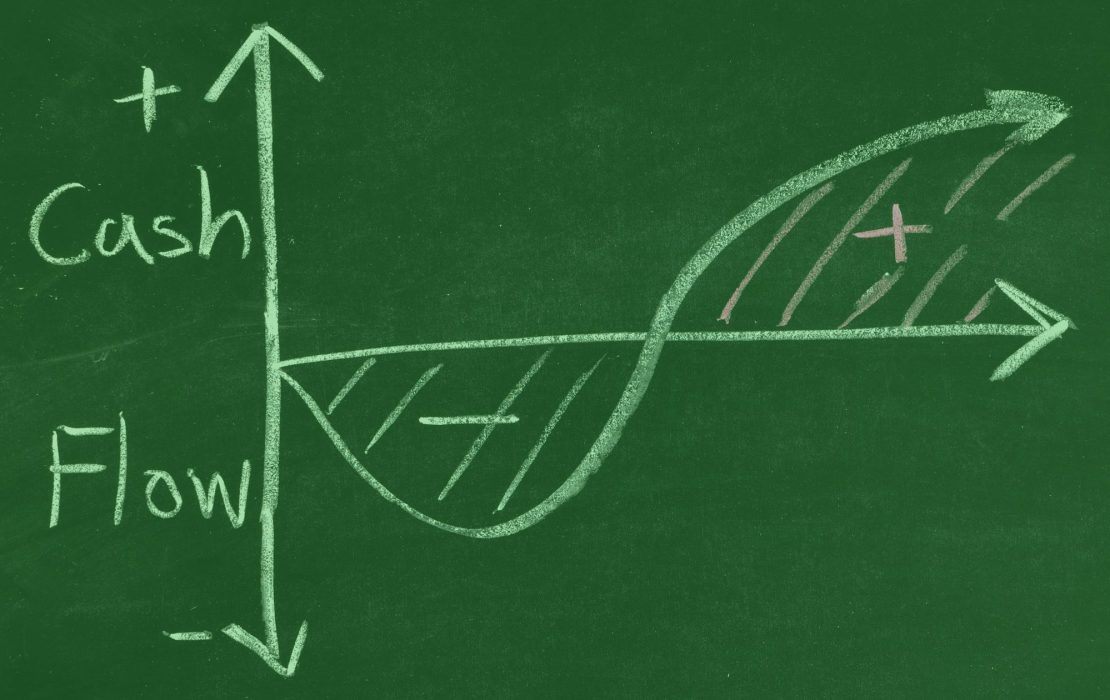

Successfully managing a business demands a delicate equilibrium of multiple factors, with cash flow as the cornerstone. Cash flow is the movement of money in...

Business owners know that it takes many cogs to ensure a well-oiled enterprise. Finding ways to improve your cash flow maintains fiscal health, which is...

journey into the known

{kind=link}