- Login

Login

Welcome back

Let's make today a great day!

Don't Have An Account Yet? Signup for free! - Who we are

- What we do

- Customer stories

- Contact us

- Login

- Sign up

- Enquire Now

As a business owner or manager, dealing with outstanding debts is an unfortunate but unavoidable part of operations. However, it’s crucial to approach debt collection compliantly to protect your rights, maintain ethical practices, and nurture valuable customer relationships. In this blog, we’ll explore the step-by-step process of legal debt collection in South Africa, shedding light on the legal framework, best practices, and debtors’ and creditors’ rights and responsibilities.

In South Africa, debt collection activities are primarily governed by the National Credit Act 34 of 2005, the Magistrates’ Court Act 32 of 1944, and the Consumer Protection Act 68 of 2008. The National Credit Regulator (NCR) oversees and regulates the debt collection industry, ensuring compliance with the law and promoting fair practices.

Before initiating the debt collection process, there are critical preparatory steps to take.

If negotiation attempts are unsuccessful, you may proceed with the debt collection process as follows:

Throughout the debt collection process, it’s essential to understand the rights and responsibilities of both debtors and creditors.

Debtors have the right to be treated fairly and respectfully, without harassment or intimidation. They have the right to receive accurate and detailed information regarding the debt they owe, and the right to dispute the debt if they believe it is inaccurate or unjustified.

Creditors, on the other hand, have the responsibility to adhere to legal and ethical standards, provide clear and accurate information, respect privacy and confidentiality, and properly document all communication with debtors. Creditors must refrain from engaging in abusive, deceptive, or unfair practices during the debt collection process.

By following a step-by-step approach, adhering to the legal framework, and maintaining ethical standards, you can increase your chances of successful debt recovery while protecting the rights and interests of all parties involved. Although staying compliant in your debt collection process is crucial, we believe that actively managing your client credit portfolio can help you avoid the need for debt collection altogether.

As a registered South African credit bureau, Cred-it-data has the resources, reports and expertise to ensure your client journey isn’t derailed by poor credit management. Our services also include assisting you in taking on financially secure clients and suppliers, offering comprehensive credit reports and giving you a clear picture of a supplier’s financial health, payment patterns, and credit score.

Safeguard your business’s financial well-being and reputation – partner with Cred-it-data for a comprehensive, compliant debt collection solution. Contact us today!

How Can I Improve My Company’s Credit Score?

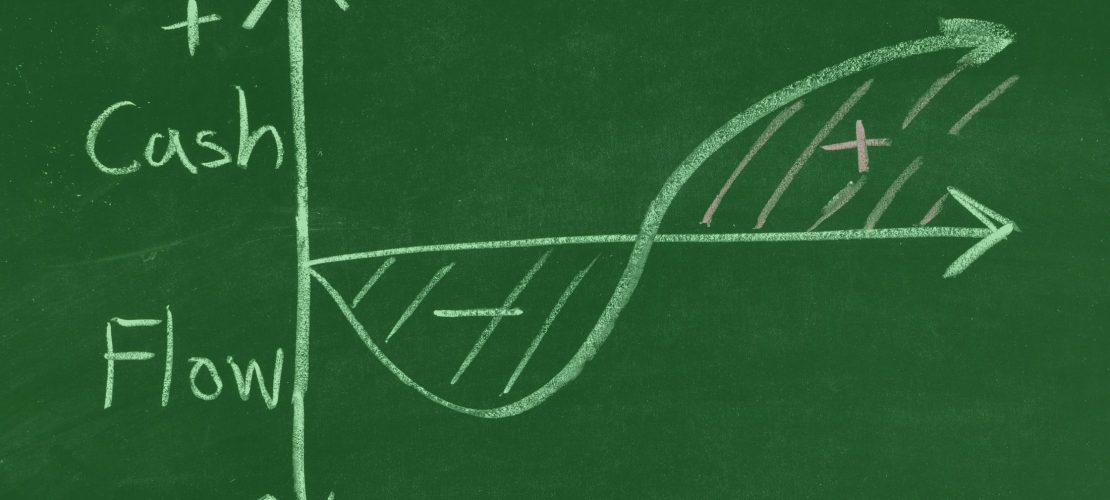

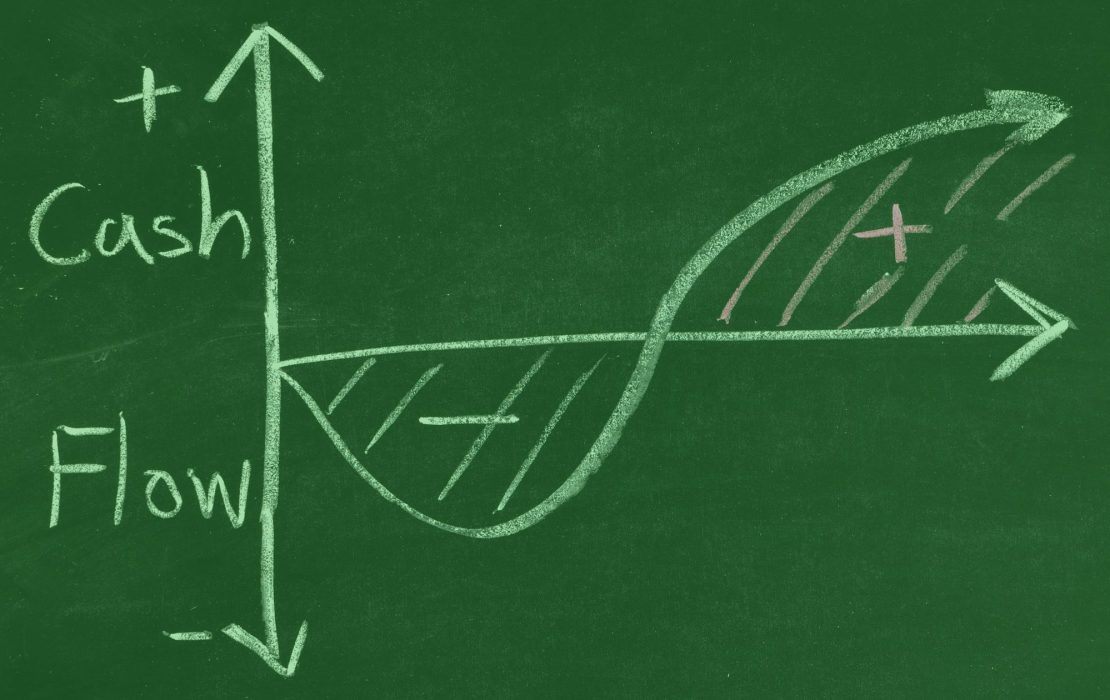

Successfully managing a business demands a delicate equilibrium of multiple factors, with cash flow as the cornerstone. Cash flow is the movement of money in...

Business owners know that it takes many cogs to ensure a well-oiled enterprise. Finding ways to improve your cash flow maintains fiscal health, which is...

journey into the known

{kind=link}